|

Curado.com

|

| Barrett, P.S. and Curado, M. T. (1996), "QUALITY AND

ENVIRONMENTAL MANAGEMENT: HOW SHOULD THE CONSTRUCTION INDUSTRY FACE NEW

PANACEAS?" in Proc. of the " CIB BEIJING INTERNATIONAL CONFERENCE QUALITY

AND ENVIRONMENTAL MANAGEMENT", BEIJING: CIB.

A QUALITY AND ENVIRONMENTAL COST MANAGEMENT SYSTEM

Francisco Loforte Ribeiro[1], Miguel Torres Curado[2], Isabel Cristina Rocha[3]

ABSTRACT: Construction companies that pay attention to quality andenvironment stay ahead the competition and survive in the modern competitive market place. A variety of tools are available to companies to help them achieve this goal. Certification to ISOs management standards, ISO 9001 and ISO 14001, has become increasingly necessary in todays global trade. ISO 10014 provides top management with information to facilitate the effective application of management principles and the selection of methods and tools that will lead the sustainable financial success of an organization. This paper focuses on managing quality and environmental costs and reaping the benefits of the ISO 9001 and ISO 14001 certifications. It discusses and presents the findings of a action research case study. It presents a computer-based quality and environment cost management system. The development of a quality and environmental cost management system requires more action research-driven approaches to cover all the relevant angles of the investigated research objectives and to generate added value by capturing construction companies real-world problems. Thus, action research (AR) method was followed for designing and developing the computer-based system presented in this paper.

KEYWORDS: CONSTRUCTION, ENVIRONMENT, PROJECTS, QUALITY, SYSTEM. introduction In the current construction markets, the concern to meet customers' requirements is added to the concern to improve economic and financial performance for the company itself. Costs, quality and environment are important aspects of construction projects for performance analysis and its linkages (Rouse and Chiu, 2009). Efficient project execution is a key business objective in many domains and particularly so for capital projects in the construction industry. The main purpose of quality and environmental management systems should always be to improve a businesss economic and financial performance (Boerner and Jeczen, 2004). Companies that pay attention to quality and environment stay ahead of the competition and survive in the modern competitive market place. A variety of tools are available to companies in order to help them achieve this goal (Ramanthan and Yunfeng, 2009). Certification to ISOs management standards, ISO 9001 and ISO 14001, has become increasingly necessary in todays global trade. These standards are built on the eight quality management principles: (1) customer-focused organizations; (2) leadership; (3) involvement of people; (4) process approach; (5) system approach to management; (6) continual improvement; (7) factual approach to decision-making; (8) mutually beneficial supplier relationships (Hele, 2003; Zeng et al., 2005). The quality and environmental management systems are the bridges that leads the customer to the product she/he wants (Nicoloso, 2007). Today, no construction company can afford to ignore the quality and environmental costs of its projects. There are many factors in the construction industry that can influence the quality and the environmental performance of construction projects, both positively and negatively, and so it is increasingly important to manage their quality and environmental costs. ISO 10014 provides top management with information to facilitate the effective application of management principles and the selection of methods and tools that will lead to the sustainable financial success of an organization. Only a few studies have so far been carried out on the integration of quality and environmental cost management systems, and this the paper presents a novel integrated model to solve this problem. This paper focuses on managing quality and environmental costs and reaping the benefits of the ISO 9001 and ISO 14001 certifications. Three case studies are discussed and a computer-based system for quality and environmental cost management is described. METHODOLOGY The development of a quality and environmental cost management system requires more action research-driven approaches to cover all the relevant angles of the investigated research objectives and to generate added value by capturing construction companies real-world problems (Alvesson, 1996). Action research (AR) takes many forms, and indicates diversity in theory and practice among action researchers, so providing a wide choice for potential appropriate actions for their research question. AR allows researchers to spend time in organizations and to research the research hypothesis on an operational basis. Thus, action research is an approach that aims both at taking action and creating knowledge or theory about that action (Coughlan and Coghlan, 2002). The researchers are professionally involved with the organizations in question (Hameria and Paatela, 2005). The strength of action research is its ability to support the creation of a new model or system, as with the development of a computer-based system for quality and environmental cost management. This made it appropriate to approach our work with action research. In addition, this approach is flexible in how it collects relevant data and aims to provide validation during the course of the systems development. Action research is collaborative and cyclical, and is described in the current literature as a recurring cycle of planning, acting, observing and reflecting (Zuber-Skerritt, 2001; Altrichter et al., 2002; Kyrö, 2004). Building on Kaplan and Norton (1993) and Neely et al. (2000) show a feasible way to develop a quality and environmental cost management system, which is characterized by expert interviews and workshops. Three construction projects of potential ones were selected for participation in this research project. In accordance with Smith and Smith (2007), these construction projects were regarded as action research case studies. They also worked as real-life case-study material in the firm. This provided first-hand experience of the problems at both firm-level and project-level, and, by interacting with the people directly involved identified potential ways of resolving them (Yee et al., 2006). In this study the approach was implemented by having two members of the research team gather data and accompany a large construction firm throughout the systems design process over a period of 11 months. The action research process was implemented in several phases. During these phases the data were gathered through workshops, from company documents, interviews conducted with various groups (including managers and employees), within the project organization and from field notes made during the assignment. The interviews collect field data for empirical modeling (Humphreys et al., 1996) in order to select relevant data and information artifacts from the list of potential items. On the basis of the literature reviews and workshop discussions, the authors developed a template for conducting case studies and writing case description of selected construction projects. Twenty semi-structured interviews were conducted, aimed at collecting information about the entire operating process of the quality and environmental management system (QEMS) in a construction project. To guide the interviews, a paper based questionnaire with open and closed questions was developed on the basis of literature research (Goldman et al. 1995) and presented at all interviews. The interviews were preceded by visits to the selected projects which included informal conversations with potential informants. The existing practices under the QEMS in the construction site were analyzed, including the overall characterization of quality and environmental management processes with respect to the plans, procedures, records and control as well as the management of costs supported by this system. The semi-structured interviewsare split between into several sections with distinct goals. There is a section on the characterization of the subject, another one focused on measuring and recording the costs in the system and a third one that approaches nonconformance and complaints. There is a section responsible for analyzing the benefits of the QEMS, a section which studies the status quo of information and communication, another one that introduces the topic of performance and improvement indicators. Finally, the subjects are presented with additional suggestions. THEORETICALBACKGROUND The implementation and certification of quality (ISO 9001) and environmental (ISO 14001) systems has become an important activity (Zeng et al., 2007). Some research studies have focused on the benefits and effectiveness of quality and environmental management systems (Petroni, 2001; Boulter and Bendell, 2002; Zwetsloot, 2003; Arauz R. and Suzuki H., 2004; Briscoe et al., 2005; Johansson and Palmes, 2005; Poksinska et al., 2006; Khan, 2008; Tsai and Chou, 2009). For example, Poksinska et al., (2006) shows that an external benefit of implementing ISO 9001:2000 is improved customer relations; the internal benefits most often mentioned relate to the standardization of organizational processes. Petroni (2001) states that implementation of ISO 14001 and subsequent registration can facilitate progress towards increased market share, improved working climate and customer satisfaction, improved efficiency of operations and processes, and cost reduction. Johansson and Palmes (2005) note that quality programs, viewed as an investment, can be assessed in financial terms at each phase of their cycle. Khan (2008) points out that, ISO 14001 or ISO 9001 certified companies around the world insist that certification is a prerequisite for business relationships. Tsai and Chou (2009) note that ISO 9001 standard has contributed to better quality, greater customer satisfaction, and higher profits and ISO 14001 standard has contributed to better environmental performance, greener products, and more transparency for and acceptance by external environmentally concerned stakeholders. Other studies, meanwhile, have focused on integrating two or three management systems from various viewpoints (Karapetrovic and Jonker, 2003; Dubinski et al., 2003; Low and Pong, 2003; Labodova, 2004; Zeng et al., 2005; Jørgensen et al. 2006). The integration of the quality and environment systems creates better chances of saving costs, improving effectiveness and achieving economic and financial benefits by allowing the synergy of tasks within the two systems - unique and integrated strategies, compatible goals and a single standard regarding for product and service consistency (Ofori et al., 2002; Salomone, 2008). From many different angles and in any construction company, the achievement of financial and economic benefits from organizational assets and resources is a key factor for staying competitive in the current markets. An organization with an effectively and efficiently implemented QEMS will not see continuous improvement if it disregards the actual costs inherent to this system and the savings/costs performance indicator figures that assess the benefits gained from it (Ribeiro, 2000). The first articles published that addressed quality costs systems date back to 1961 with Feigenbaum being one of the first to classify them according to the current method of categorization: prevention, assessment and failures (PAF). In 1974, this concept was approached by the American Society for Quality Control and in 1979 by Crosby (Wang and Guo, 2007). The NP 4239:1994 standard establishes an important foundation and guidelines for the quantification of quality costs, and it even provides measures for improving productivity. The appearance of failure mode and effects analysis (FMEA) has been welcomed and applied in a wide range of industries such as aerospace, nuclear, chemical and manufacturing (Chin, et al. 2009). The FMEA technique aimed at to define, identify and eliminate known and/or potential failures, problems, errors from the system, design, process and/or service before they reach the customer (Linton, 2003; Stamatis, 1995). Gilchrist (1993), following the appearance of the[10] W. Gilchrist, Modelling failure modes and effects analysis, International Journal of Quality & Reliability Management (5) (1993), pp. 1623. FMEA proposed an expected cost model which has the great benefit of forcing people to think about quality costs. A number of ways for classifying the quality and environmental costs were developed. Generally, quality and environmental costs can be classified into conformance/quality costs and non-quality/failure costs (Ireland, 1991; Sjoholt & Lakka, 1994; Sarmiento & Serppell, 1999; Holland, 2000; Love & Irani, 2003; Schiffauerova & Thomson, 2006). The quality and environmental costs derive from the effort invested in achieving quality and clean production in the given products/services. These costs can be divided into prevention costs and assessment costs. The former are the costs of activities whose aim is to ensure product/service compliance with the established requirements (planning, documentation, implementation and maintenance of the QEMS. The latter are the costs associated with activities directed at determining the degree of compliance with the requirements (tests, trials and inspections, etc.). Non-conformity costs are the result of not complying with customer and regulatory requirements. If defects or flaws are corrected during design or production they are called internal failurecosts. Repairs of errors or failures produced after the client has received the product/service are called external failure costs (Ribeiro, 2000; Schiffauerova & Thomson, 2006). The ISO 10014:2006 standard by provides guidelines for achieving financial and economic benefits through the application of eight quality management principles (ISO, 2006). In relation to economics it is relevant to highlight the ISO 10014 standard which provides guidelines for assessing the viability and profitability of the QMS (Ribeiro, 2006). Studies show that senior managements attention and focus is more easily captured when facts and figures resulting from quality improvement are presented as return on investment figures (Brad et al., 2006).However as pointed out by Choi et al. (2009) the appropriation of quality management costs and independence of the quality management organization is still unsatisfactory in the construction industry. The above discussion reveals a gap in the literature as to how construction companies manage the quality and environmental costs to become more profitable and to reap the benefits of quality and environmental management systems. It is important to bridge this gap because construction companies are concerned with this issue. Quality and environmental cost management promotes productivity and thus the competitive standing of the company in its field. The aim is to reduce failure costs and assessment costs since they do not add value to the process unlike those related to prevention (although assessment costs may sometimes contribute in by adding value to the process of production). Most large companies claim they conduct an assessment of the costs of quality. However, those costs often do not take into account all the existing costs, nor do all companies use a formal classification structure to collect all costs according to categories (Schiffauerova & Thomson, 2006). the action research case study The main purpose of this research is to develop a computer-based application for managing quality and environmental costs suitable for construction firms. OPWAY was selected for the implementation of the action research methodology. The firm OPWAY is a company formed 2007 by the merging of two major construction companies in Portugal: OPCA, 75 years old and SOPOL, 49 years old. This firm has implemented an integrated quality and environmental management system (QEMS). At the top of QEMSs documentation is a quality and environmental manual covering all of the firms organization structure. At project level are the construction contract management plans (CCMP), work schedules, work-routines, inspections and trials plans, environmental-control forms, organizational diagrams, functions and tasks description and quality plans for the certified suppliers/sub-contractors. The firm has an organized archive comprising all the quality and environmental records as required by ISO 9001:2000 and ISO 14001:2004 standards. Each CCMP assures the implementation of the quality and environmental policies and the associated quality and environmental objectives at project level in accordance with the legal and contractual requirements. A computer application based on the balanced score card method is available to all managers through the firms intranet. This application displays monthlyindicators of the overall compliance status of the QEMS processes. This program aids decision-making and monitoring the QEMS performance. In addition, it helps the firm to keep an eye its quality and environmental goals, alerting too any deviations from pre-determined performance targets. The three selected projects were all under construction and all of them have implemented a documented CCMP. There were twenty semi-structured interviews with project managers, environment and quality technicians, quality and environment directors. The most immediate finding from interviewees is that OPWAY assigns much importance to the financial value quality and environmental non-conformances. The costs handled by the QEMS and which are accounted for by OPWAY are the costs of failures, which includes the non-conformities and complaints. The majority of non-conformities are detected during the execution and accounted in monthly periods. Non- conformities have a considerable impact on project cost and time. The interviewees were of opinion that management effort should mostly be directed towards the prevention of failure to reduce costs in future works. They also agree with the need to change the way complaints are handled, to take a more proactive approach along with the creation of a users manual. Most of the interviewees stressed the importance of the performance indicators which allow them to assess the QEMS effectiveness each month. But the interviewees agreed that there is no way to track and assess the quality and environmental cost of their projects. Most of non-conformities are associated with subcontracted works. the proposed quality and environmental management system The quality costs models found in the bibliography proved to be too broad in terms of their practical application and, therefore they had to be adjusted. The case study action research helped the authors to develop a quality and environmental cost structure adjusted to the nature of construction projects. The cost structure used in the research work, like those found in the reference bibliography, was split into two groups: 1) costs of conformity; and 2) costs of non-conformity (Table 1). The costs of achieving conformity are subdivided into prevention costs and the cost of assessment at firm and project levels. The costs of non-conformity are subdivided into the cost of internal failures and cost of external failures. Table 1: Cost structure

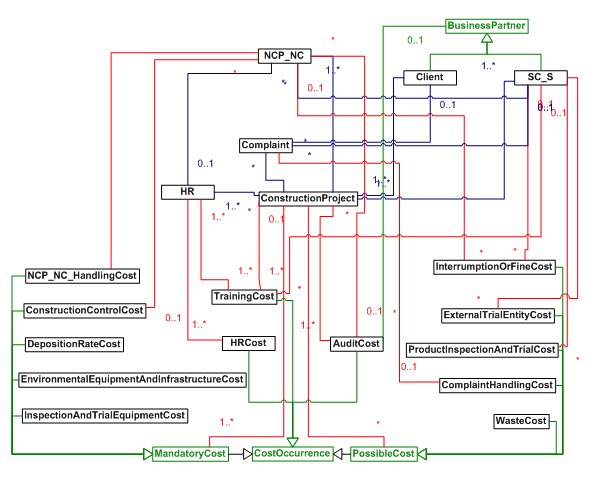

A distinction was made between costs that only relate to the firm's operations (F) and costs directly linked to the construction projects (P). External training involves all employees not deployed to any construction projects. Internal training and audits involve people from certain departments within the firm and people pertaining the projects organizations. In the latter case, the corresponding costs pertain to the construction project in question, despite being accounted simultaneously as company costs. The same applies to human resources costs for employees operating from headquarters and dealing with some or all ongoing construction projects. The UML language (Unified Modeling Language) was used in the specification and design of the proposed model. This modeling language can be used build a representation and specification of the components of a computer based system (Korth et al., 2002). The UML Class Diagram was chosen for development of the conceptual model. This conceptual model describes the static structure of the system with objects (entities) characterized by attributes and operations. Figure 1 presents a view of such specification.The business partner consists on an abstract entity generalization which can be specialized as Client and SC_S (Subcontractor or Suppliers). The Client represents an entity which can file Complaints, can award Construction Project and can be the auditor in relation to an Audit Cost. A Construction Project represents ongoing construction works and those works already delivered but still within the warranty period. The Construction Project is an entity to which human resources (HR) are assigned (quality and environment employees). Construction Projects may be the target of Complaints and be associated with Non-conformant Product (NCP) or Non-conformity (NC). It also has a Client and one or more Sub-contractors and Suppliers (SC&S) (two independent relations in the diagram). The project includes Training Costs for its employees as well as Audit Costs (two independent relations). Lastly, all specializations of Mandatory Costs are associated with one Construction Work and may or may not be associated with the specializations of Eventual Costs.

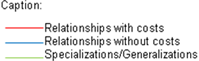

Figure 1: Conceptual model An NCP_NC may have the responsibility of an SC_S or of an HR. Each NCP_NC occurs in a Construction Project. This entity may result from a work-control cost or from an audit (two independent relations) and is linked to a cost of handling an NCP. The occurrence of such costs may or may not cause interruption costs or fines. Based on the specification, a computer based system was developed. Figure 1 describes its high-level architecture. The developed systems aim is to support quality and environment cost management in the construction industry. It should support consultation, insertion, updating and deletion of stored information as basic support operations available to any quality and environment technician and project manager (construction site), or director of quality and environment (company headquarters). To implement this system, a Microsoft SQL database application was developed for storing both the conformity quality and environmental costs and non-conformity quality and environmental cost. These costs can be registered in such a way that they could be associated with the corresponding process or activity in a given construction project. As a supplement, comparative indicators were created to facilitate comprehension and allow a more in-depth cost analysis.

Figure 2: Systems architecture |

|

||||||||||||||||||||||||||||

The system is functionally divided into two sets of components: the quality and environmental cost database (QECDB) and the quality and environmental cost management system (QECMS). The latter component includes a user interface. The user interface navigation between pages and forms was made possible with the creation of a switchboard (control panel). The system can provide cost reports that include a set of performance indicators to aid decision-making and the discovery of sources of waste or causes of non-conformance. For a given construction project, the following indicators are calculated:

§Prevention Indicator (total prevention costs / construction project budget);

§Failure Indicator (total failure costs / construction project budget);

§QEMS Indicator (total costs / construction project budget).

In the global reports, the following indicators are calculated and shown:

§Prevention indicator (total prevention costs / total QEMS costs);

§Failure Indicator (total failure costs / total QEMS costs).

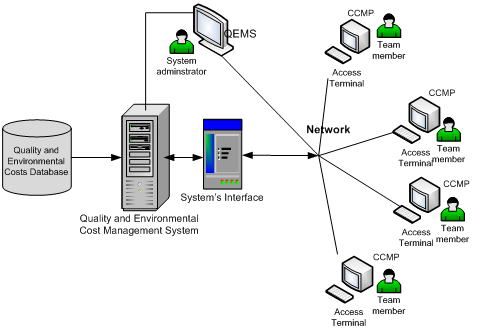

Figure 3 shows one of the forms for editing and viewing the costs of a clients complaint during the warranty period.

![]()

Figure 3: A complaint form

The proposed system was tested by applying it to several real cases to evaluate the functionality of the program in the form of representative examples. Manual tests were carried out on the interface, functions and data flow, simulating daily usage in a real context with the participation of several professionals. This was supplemented with the creation of summarized cost reports for the QEMS. The testing and validating of the software application was conducted simultaneously with a constant search for flaws or improvement opportunities. Testing the many components of a software program is essential in these stages, and it can be assumed that the verification and the testing of software applications is included within the concept of software validation. This applications verification and validation not only considered each of its components individually but it also analyzed the application as a whole, considering the models from the designer and user perspectives (Jagdev et al., 1995).

The QECMS was tested repeatedly through several stages until the system reached a state that assured the validity of the proposed model. The tests comprised manual inspections and validation, focusing on the programs expected functionality according to the requirements, the programming techniques used to achieve expected performance and reliability and ergonomics according to future usage situations (Greif, 2006).

Conclusions

This paper describes a computer-based system for managing quality and environmental costs in the construction industry. The system tasks are derived from the provisions in the ISO 9001 and ISO 14001 standards and designed to be integrated with other computer-aided project management functions through the firms network. A conceptual model was defined to represent the information used in the system tasks based on three action research cases within the real environment of a large construction firm. The developed system will render the assisted quality and environmental management tasks more effective. Its use was tested on data from different construction domains. It is an essential performance assessment tool for the QEMS. The authors followed up usage and usefulness during the systems implementation. It enables action based on concrete results and data and thus supports the continuous improvement of the management system a point highlighted as essential in all normative documents in this field of work and which completes the plan-do-check-act (PDCA) cycle.

For the quality and environment research area, our study will hopefully encourages more research on real cost management applications in the construction industry. Finally, we must acknowledge the limitations of our work since there is a need to take the development of the proposed model further.

References

Altrichter H., Kemmis S., McTaggart R. and Zuber-Skerritt O. (2002, The concept of action research, The Learning Organization 9 (3), pp. 125131

Alvesson M. (1996), Leadership studies: From procedure and abstraction to reflexity and situation, Leadership Quarterly, 7 (4), pp. 455485.

Arauz R. and Suzuki H. (2004), ISO 9000 performance in Japanese industries, Total Quality Management 15 (1), pp. 333.

Beynon W., Rasmequan S. and Russ S. (2002), A new paradigm for computer-based decision support, Decision Support Systems33, pp. 127142.

Boerner G. and Jeczen A. (2004), Linking Integrated Management System with Maslows Pyramid of Human Needs, ISO Management Systems, 4 (3), pp. 31-35.

Boulter L. and Bendell T. (2002), How can ISO 9000:2000 help companies achieve excellence? What the company think?, Measuring Business Excellence, 6 (2), pp. 3741.

Brad, S., Fulea, M., & Mocan, B. (2006), Expert System for Quality Cost Planning, Monitoring and Control, Technical University of Cluj-Napoca.

Briscoe J.A., Fawcett S.E. and Todd R.H. (2005), The implementation and impact of ISO9000 among small manufacturing enterprises, Journal of Small Business Management, 43 (3), pp. 309330.

Chin K.S, Wang Y-M, Poon G. K. and Yang J-B (2009), Failure mode and effects analysis using a group-based evidential reasoning approach, Computers and Operations Research, 36 (6), pp. 1768-1779.

Choi M, Brand M. and Kim J. (2008), A feasibility evaluation on the outsourcing of quality testing and inspection,International Journal of Project Management, 27 (1), pp. 89-95.

Coughlan P. and Coghlan D. (2002), Action research for operations management International Journal of Operations & Production Management, 22 (2), pp. 220-240.

Dubinski J. Gruszka E. and Krodkiewska-Skoczylas (2003), E. Integrating management systems? No problem for pioneering Poles!, ISO Management Systems, 3 (2), pp. 43-50.

Gilchrist W. (1993), Modelling failure modes and effects analysis, International Journal of Quality & Reliability Management, 10 (5), pp. 1623.

Goldman, S.L., Nagel, R.N. & Preiss, K. (1995), Agile Competitors and Virtual Organizations: Strategies for Enriching the Costumer. New York: Van Nostrand Reinhold.

Greif, N. (2006), Software testing and preventive quality assurance for metrology. Computer Standards & Interfaces, pp. 286-296.

Hameria A.P. and Paatela A. (2005), Supply network dynamics as a source of new business, International Journal of Production Economics, 98, pp. 4155.

Hele, J. (2003), The Eight Quality Management Principles a practical approach ISO Management Systems, 3 (2), pp. 36-40.

Holland, N.L. (2000), A construction quality cost tracking system - Implementation of construction quality and related systems, CIB-TG36.

Humphreys, P., Bannon, L., McCosh, A., Migliarese P. and Pomerol J.-C. (1996), Implementing systems for supporting management decision: Concepts, methods and experiences, Chapman & Hall, London.

Ireland, L. (1991), Quality Management for projects and programs, Project Management Institute.

ISO (2006), ISO 10014: 2006, Quality management Guidelines for Realizing financial and economic benefits, ISO Copyright Office, Geneva.

Jagdev, H. S., Browne, J., and Jordan, P. (1995), Verification and validation issues in manufacturing models. Computers in Industry, pp. 331-353.

Johansson T.J.and Palmes C. (2005), Show me the money! How quality management systems affect the bottom line, ISO Management Systems, 5 (2), pp. 17-19.

Jørgensen T.H., Remmen A. and Mellado M.D.(2006), Integrated management systems three different levels of integration, Journal of Cleaner Production 14 (8), pp. 713722.

Kaplan R. and Norton D. (1993), Putting the balanced scorecard to work, Harvard Business Review 71 (5), pp. 134147.

Karapetrovic S. and Jonker J. (2003), Integration of standardized management systems: Searching for a recipe and ingredient, Total Quality Management and Business Excellence, 14 (4), pp. 451459.

Khan Z. (2008), Cleaner production: An economical option for ISO certification in developing countries, Journal of Cleaner Production, 16 (1), pp. 2227.

Korth, H. F., Sudarshan, S., & Silberschatz, A. (2002), Database System Concepts (4th ed.), New York: McGraw-Hill.

Kyrö P. (2004), Benchmarking as an action research process, Benchmarking: An International Journal, 11 (1) pp. 5273.

Labodova A. (2004), Implementing integrated management systems using a risk analysis based approach, Journal of Cleaner Production12 (6), pp. 571580.

Linton J.D. (2003), Facing the challenges of service automation: an enabler for e-commerce and productivity gain in traditional services, IEEE Transactions on Engineering Management, 50 (4), pp. 478484.

Love, P. E., & Irani, Z. (2003) A project management quality cost information system for the construction industry Information & Management, 40, 649-661.

Low S.P. and Pong C.Y. (2003), Integrating ISO 9001 and OHSAS 18001 for construction, Journal of Construction Engineering and Management, 129 (3), pp. 338347.

Neely A., Mills J. et al. (2000), Performance measurement system design: Developing and testing a process-based approach, International Journal of Operations and Production Management, 20 (10), pp. 11191145.

Nicoloso, E. (2007), Bridging the gap between quality management systems and product quality, ISO Management Systems, 7 (1), pp. 7-11.

Ofori, G., Gang, G., & Briffett, C. (2002), Implementing environmental management systems in construction: lessons from quality systems, Building and Environment (37), pp. 1397-1407.

Petroni A. (2001), Developing a methodology for analysis of benefits and shortcomings of ISO 14001 registration: Lessons from experience of a large machinery manufacturer, Journal of Cleaner Production, 9 (4), pp. 351364.

Poksinska, B., Eklund, J.A.E. and Dahlgaard, J.J. (2006), ISO 9001:2000 in small organizations Lost opportunities, benefits and influencing factors, International Journal of Quality and Reliability Management23 (5), pp. 490512.

Ramanthan, R. and Yunfeng J. (2009), Incorporating cost and environmental factors in quality function deployment using data envelopment analysis, Omega, 37 (3), pp.711-723.

Ribeiro, F.L. (Dezembro de 2000). O controlo de custos da qualidade - Uma abordagem pelo custo global, Betão, pp.49-54.

Ribeiro, F. L. (2006), Gestão da economia da qualidade. In LNEC, Encontro nacional sobre qualidade e inovação na construção - QIC , pp. 253-260, Lisboa: Laboratório Nacional de Engenharia Civil.

Robson C. (2002), Real World Research (second ed.), Blackwell Publishing.Narasimhan.

Rouse P. and Chiu T. (2009), Towards optimal life cycle management in a road maintenance setting using DEA, European Journal of Operational Research, 196 (2), pp. 672-681.

Salomone R. (2008), Integrated management systems: experiences in Italian organizations. Journal of Cleaner Production (doi:10.1016/j.jclepro.2007.12.003), pp. 1-21.

Sarmiento A., & Serppell A. (1999). Implantation de un sistema del costos de calidad en proyetos de construccion, Revista Ingeniería de Construcción, 20 , pp. 54-62.

Schiffauerova A., & Thomson V., (2006). A review of research on cost of quality models and best pratices, International Journal of quality and reliability management , 23 (4).

Sjoholt O. and Lakka, A. (1994), Measuring the results of quality improvement work, NBRI.

Smith M. and Smith D. (2007), Implementing strategically aligned performance measurement in small firms, International Journal of Production Economics, 106, pp. 393408.

Stamatis D.H. (1995), Failure Mode and Effect Analysis: FMEA from Theory to Execution, ASQC Quality Press, Milwaukee, Wisconsin.

Tsai W-H and Chou W-C (2009), Selecting management systems for sustainable development in SMEs: A novel hybrid model based on DEMATEL, ANP, and ZOGP, Expert Systems with Applications, 36 (2), pp. 1444-1458.

Tsim Y.C., Yeung V.W.S. and Leung E.T.C. (2002), An adaptation to ISO 9001:2000 for certified organizations, Managerial Auditing Journal 17 (5), pp. 245250.

Wang, Q.-e. and Guo, X.-m., (2007), A Study of Supplier Selection and Quality Strategy Based on Quality Costs Theory, 14th International Conference on Management Science & Engineering, pp. 1-6. China.

Yee C., Tan K. and Platts K. (2006), Managing downstream supply network: A process and tool, International Journal of Production Economics, 104, pp. 722735.

Zeng S.X., Shi J.J. and Lou G.X. (2007), A synergetic model for implementing an integrated management system: An empirical study in China, Journal of Cleaner Production, 15 (8), pp. 17601767.

Zeng S.X., Tian P. and Shi J.J. (2005), Implementing integration of ISO 9001 and ISO 14001 for construction, Managerial Auditing Journal, 20 (4), pp. 394407.

Zuber-Skerritt O. (2001), Action learning and action research: Paradigm, praxis and programs. In: S. Sankaran, B. Dick et. al. Editors, Effective Change Management Using Action Research and Action Learning: Concepts, Frameworks, Processes and Applications, Southern Cross University Press, Lismore, Australia.

Zwetsloot G.I.J.M. (2003), From management systems to corporate social responsibility, Journal of Business Ethics, 44 (2/3), pp. 201207.